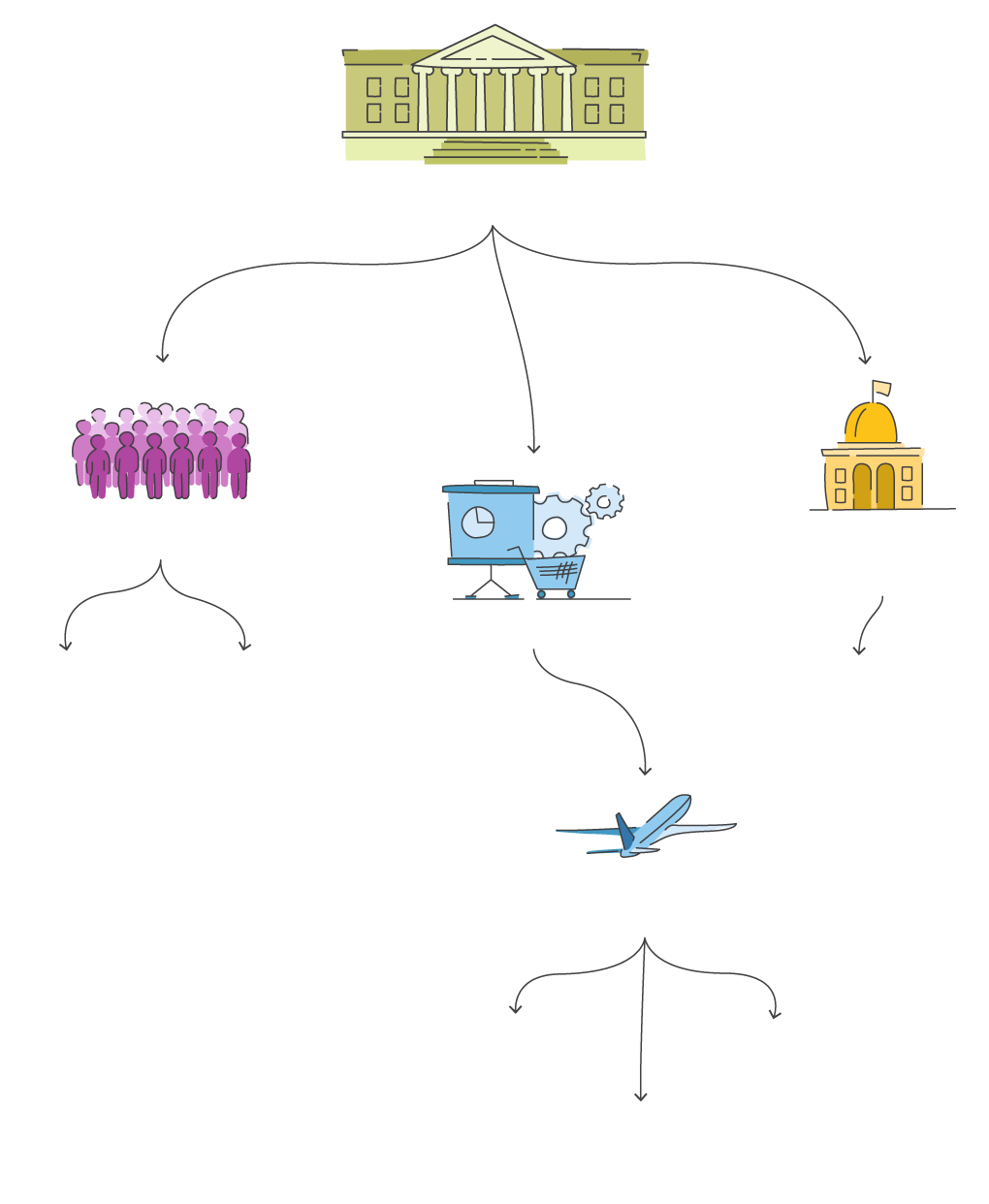

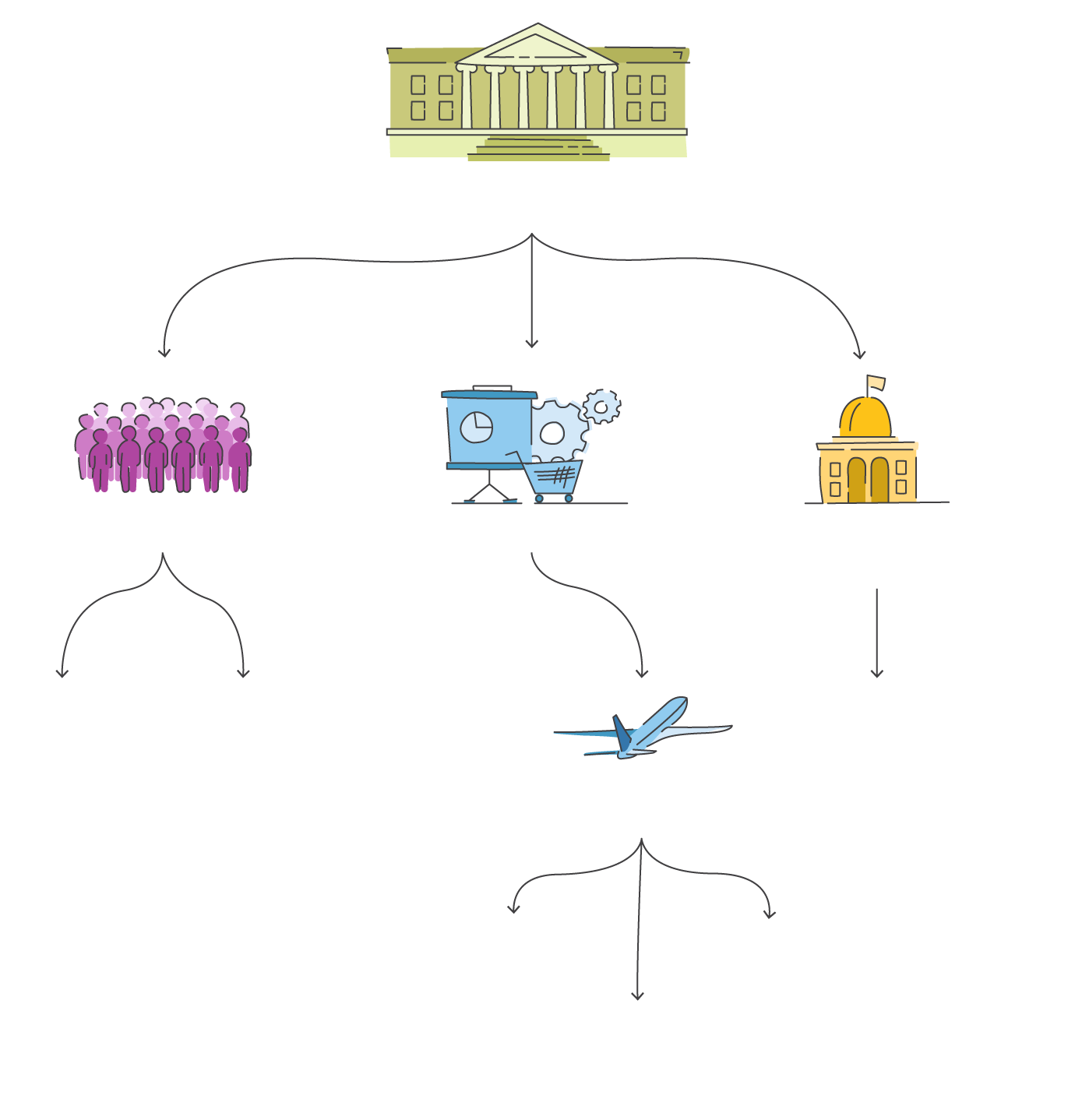

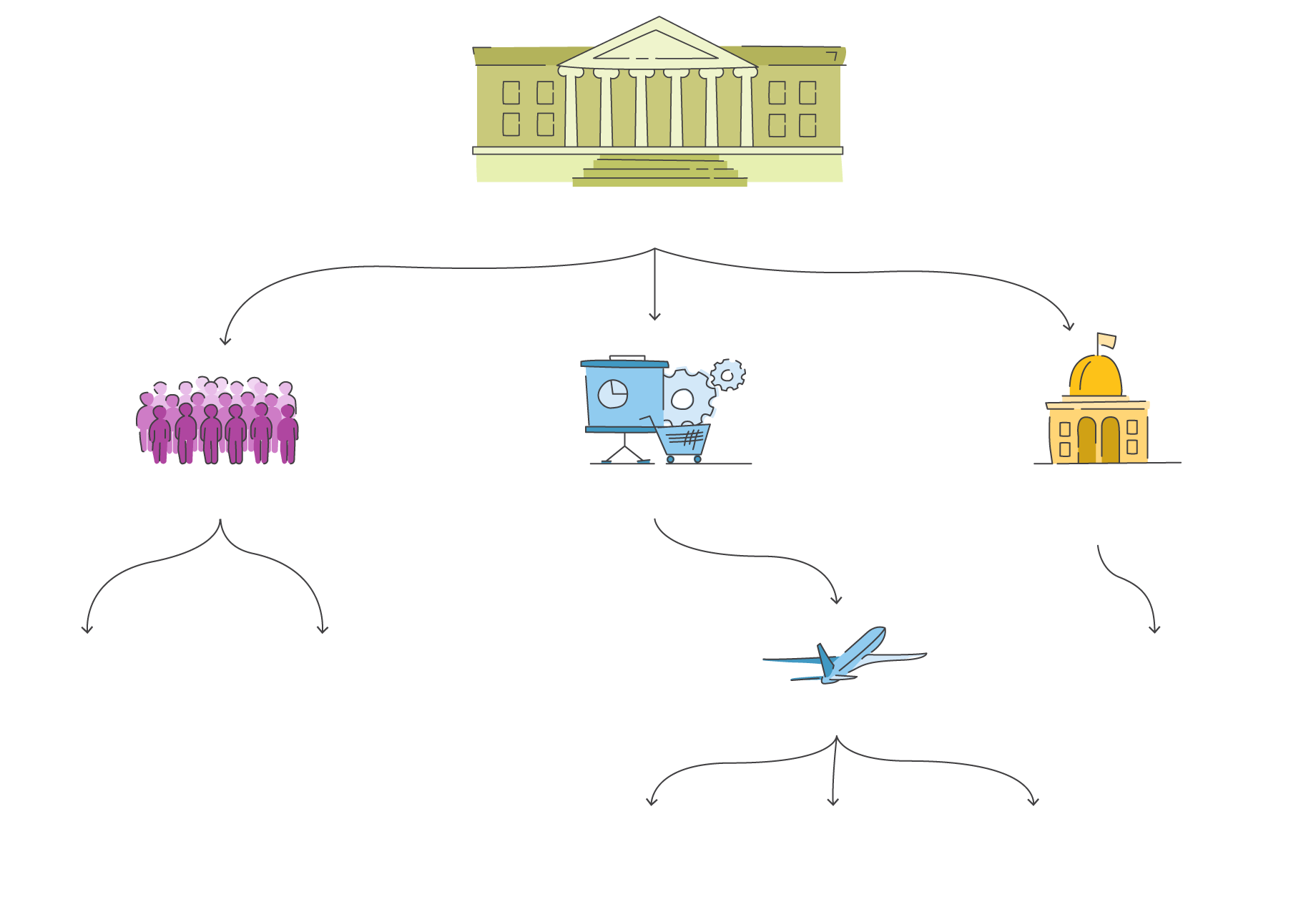

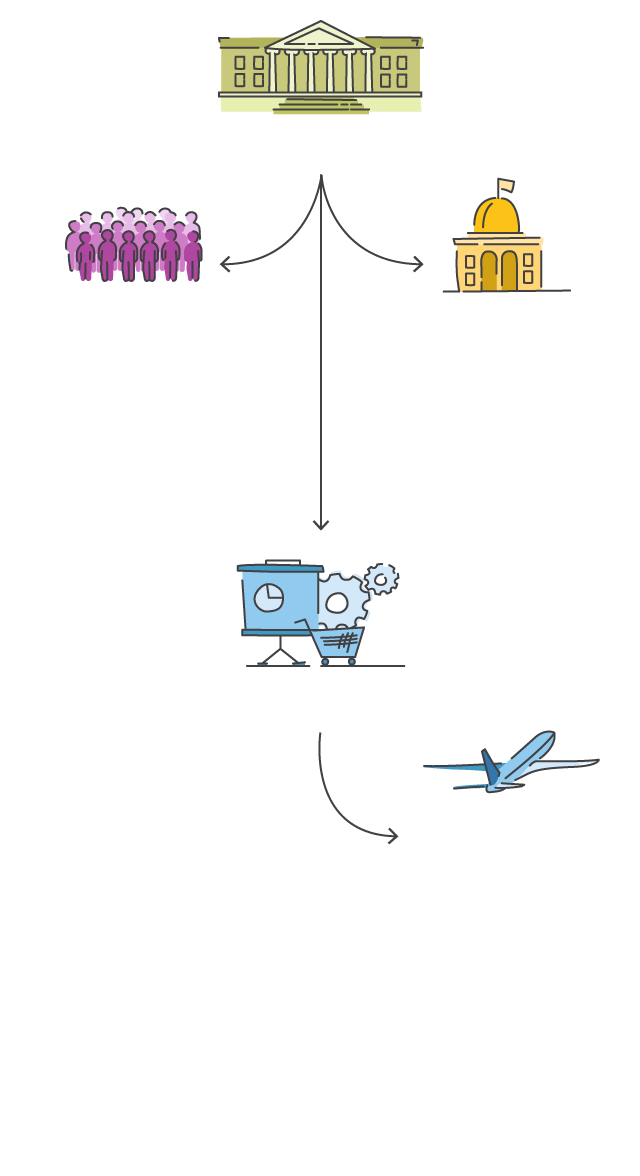

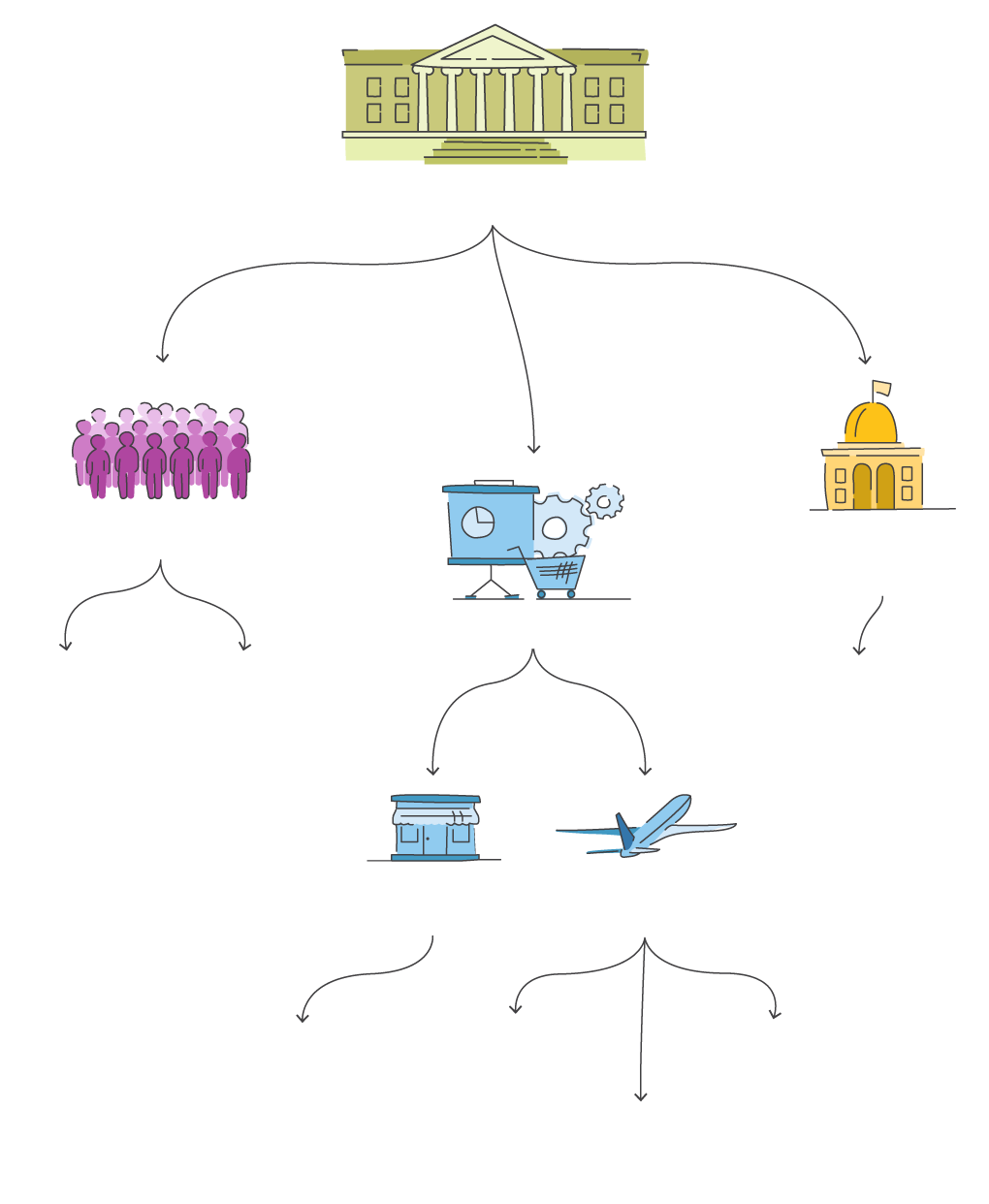

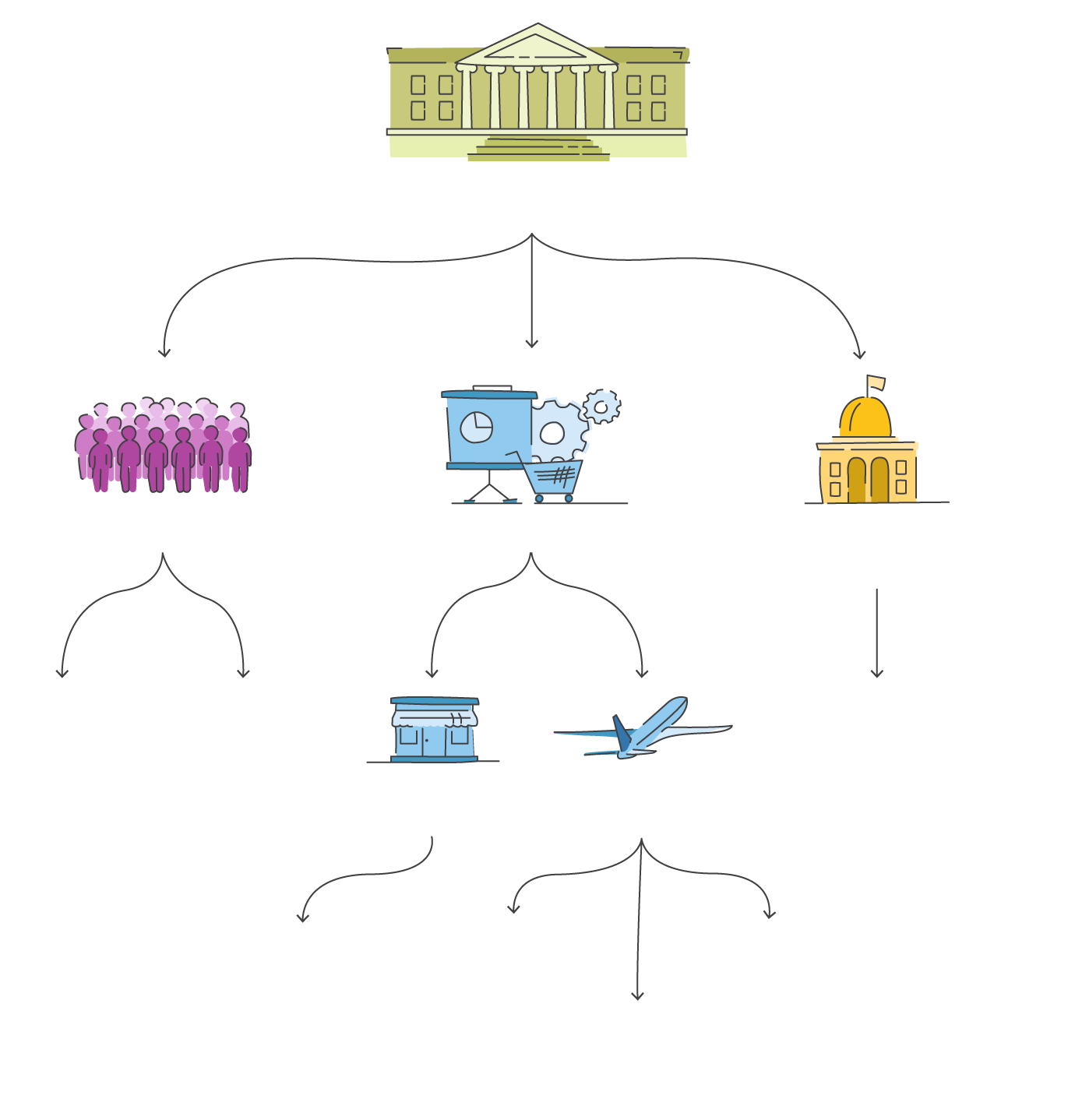

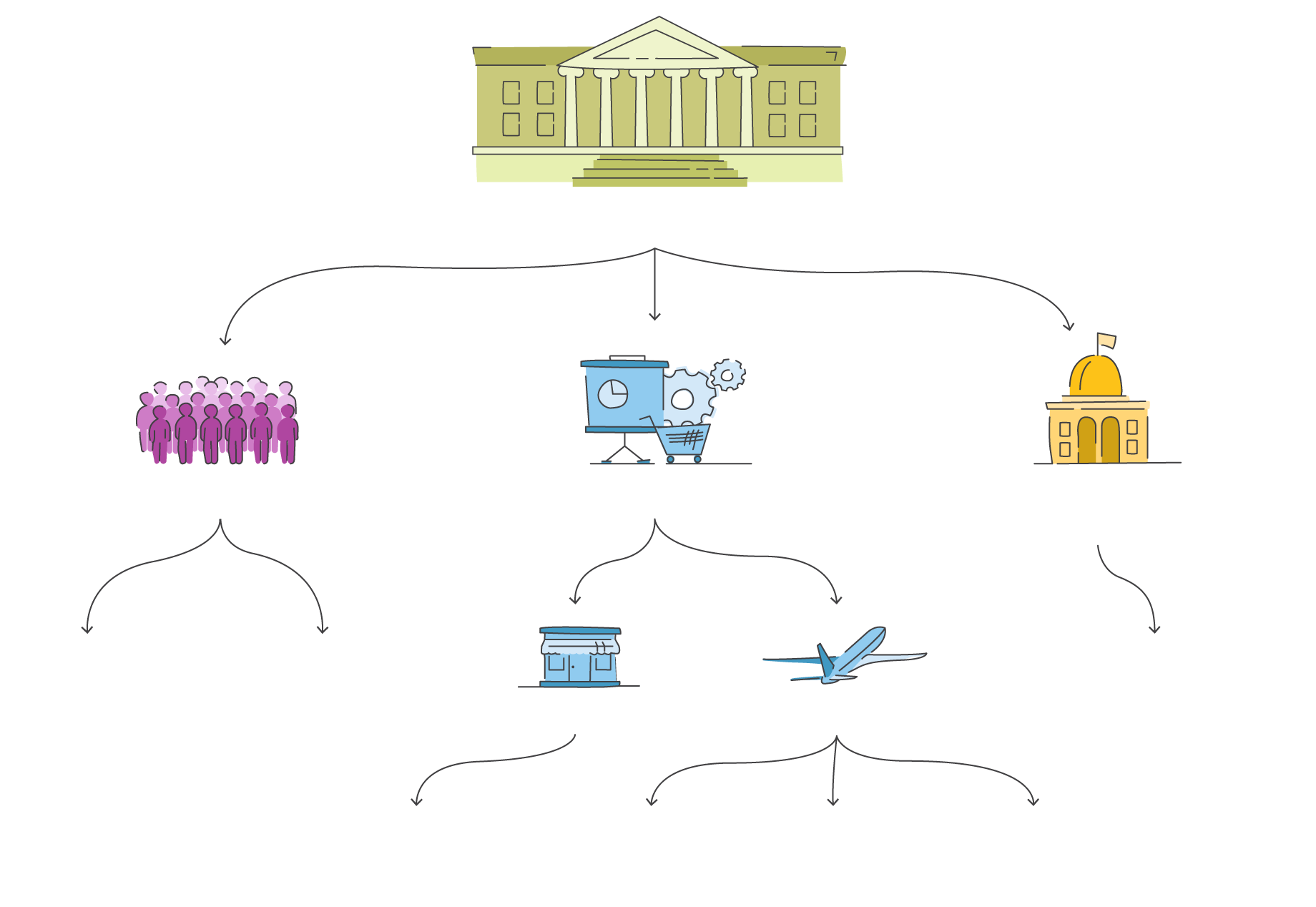

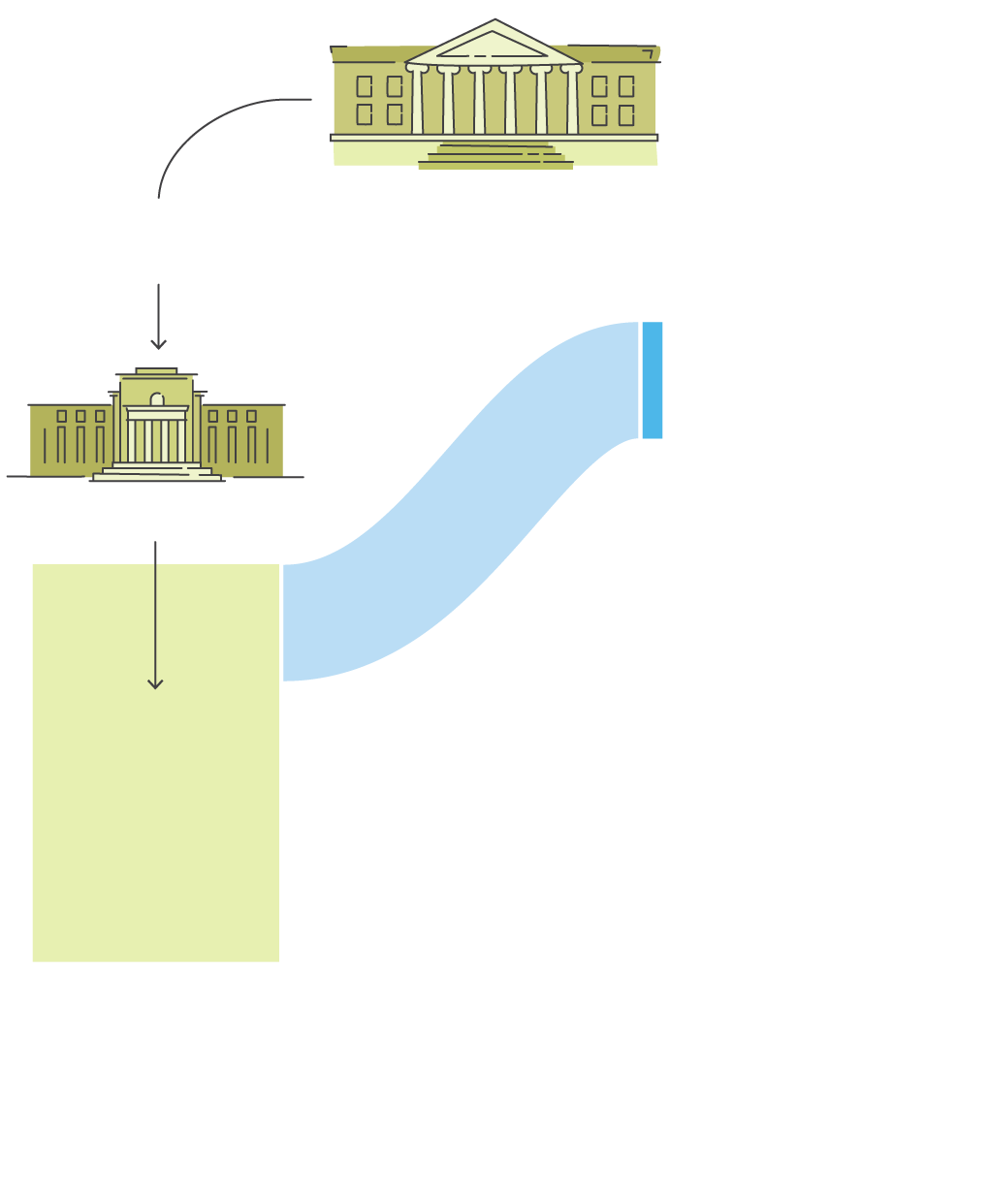

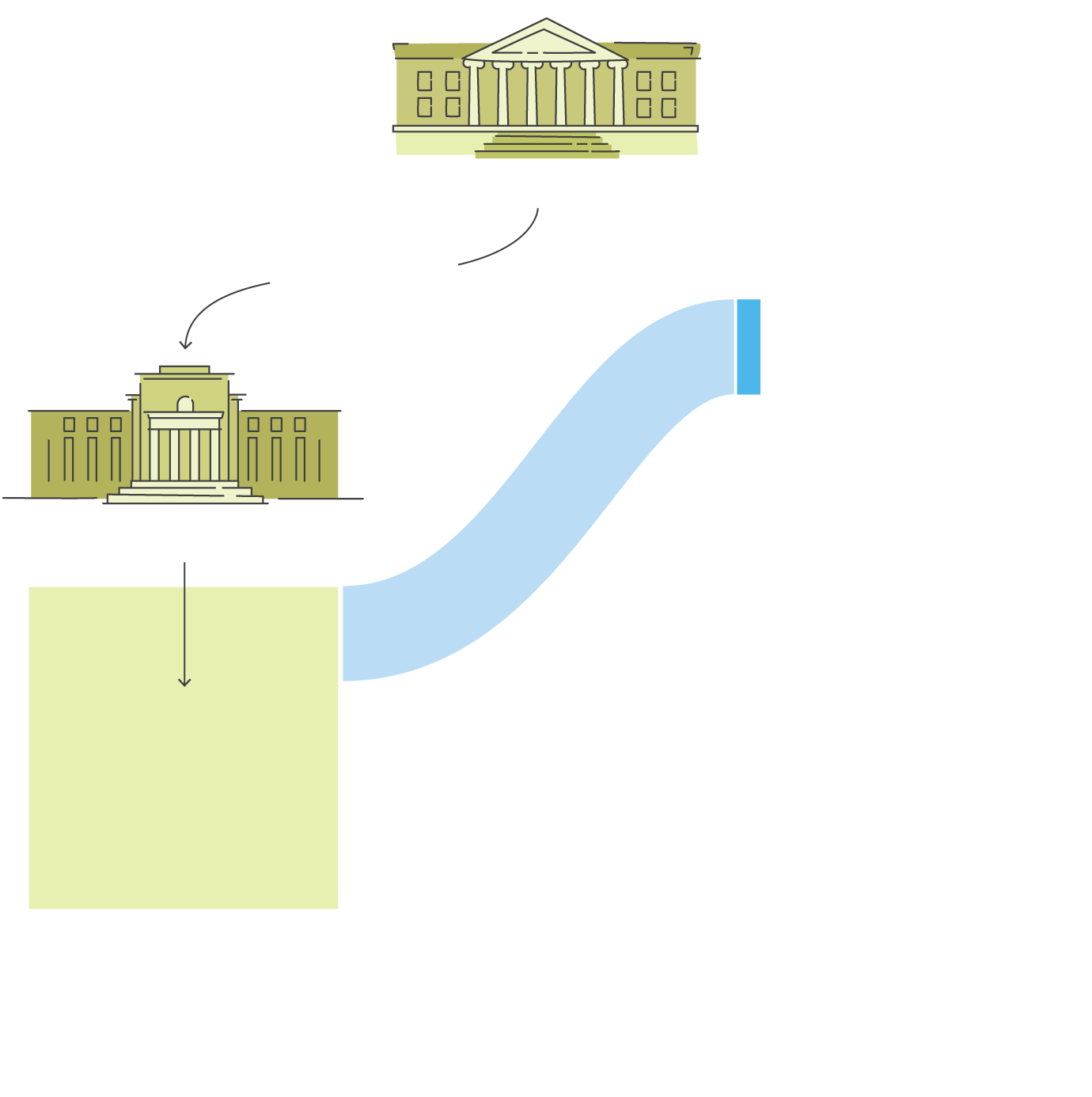

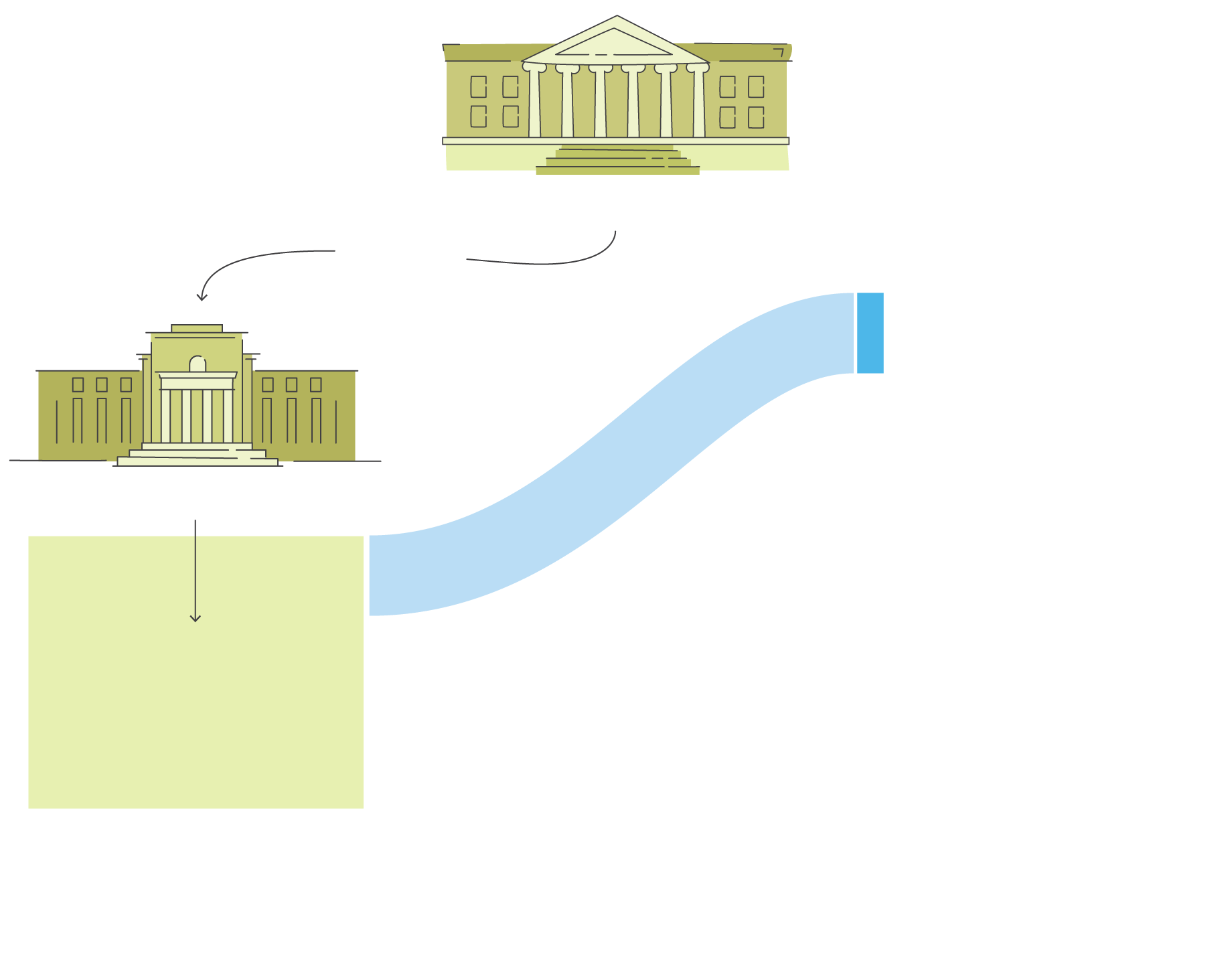

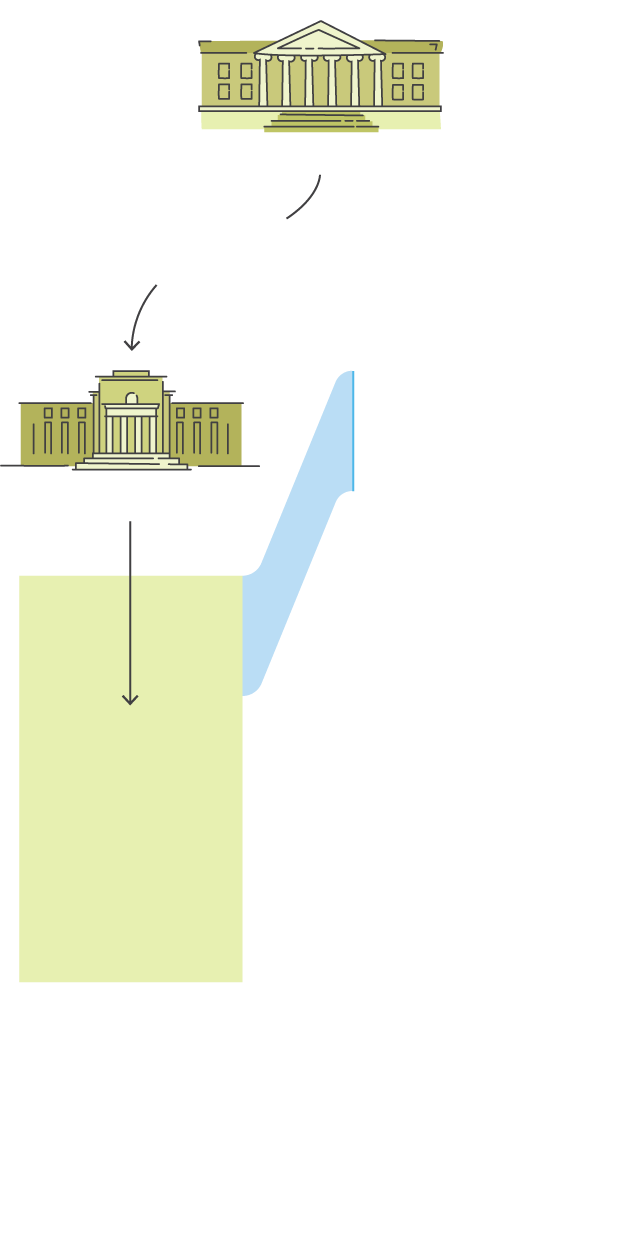

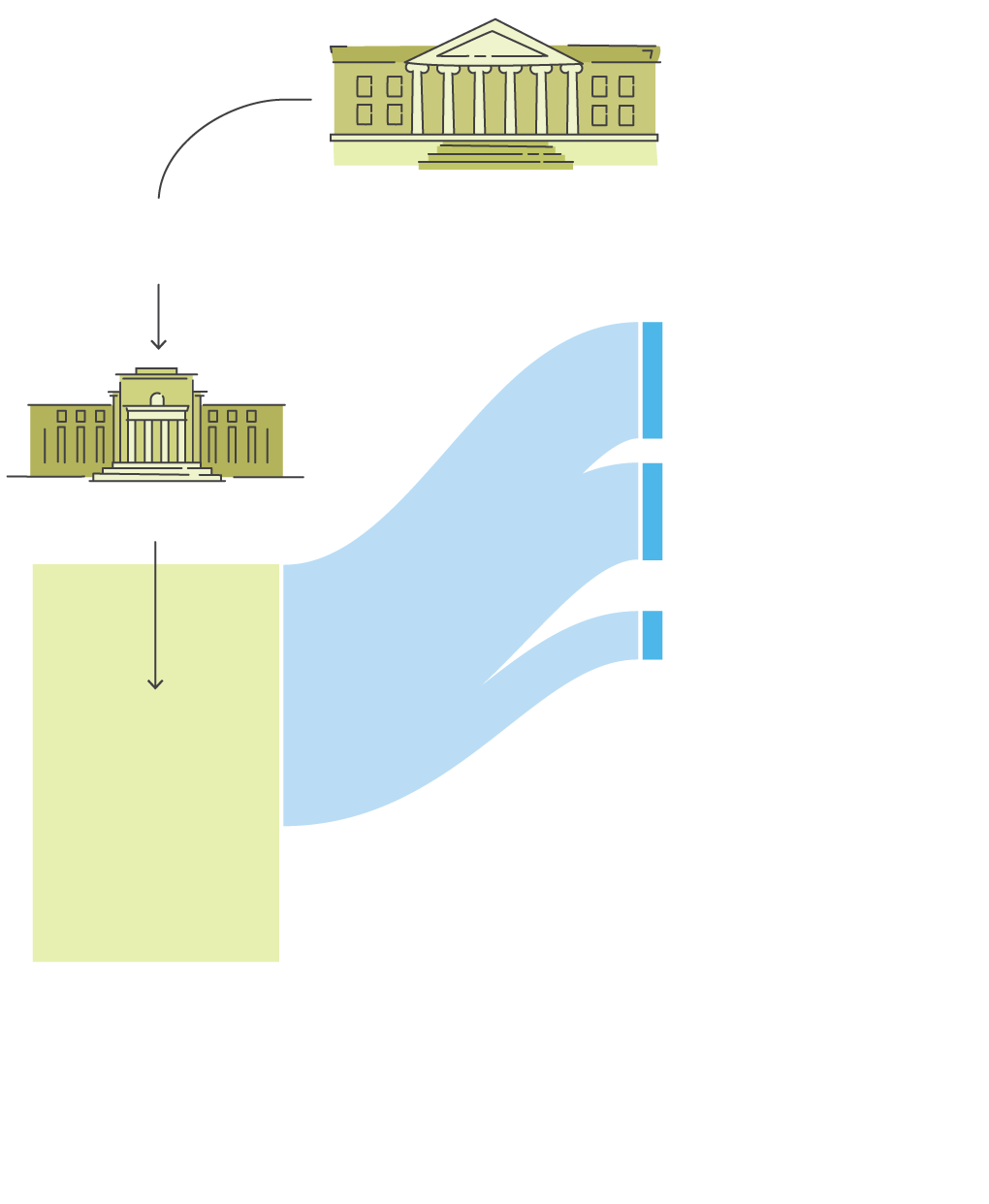

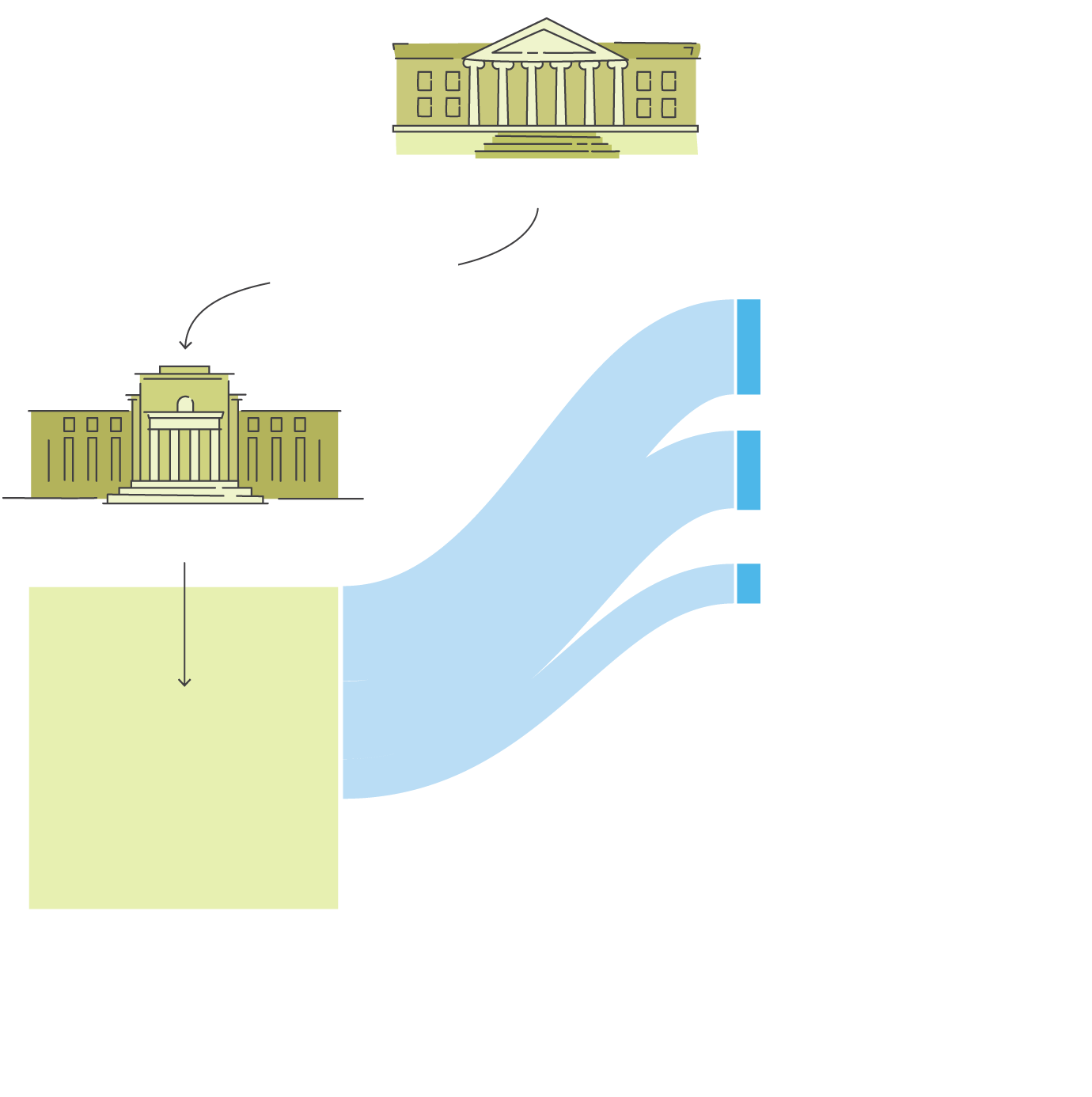

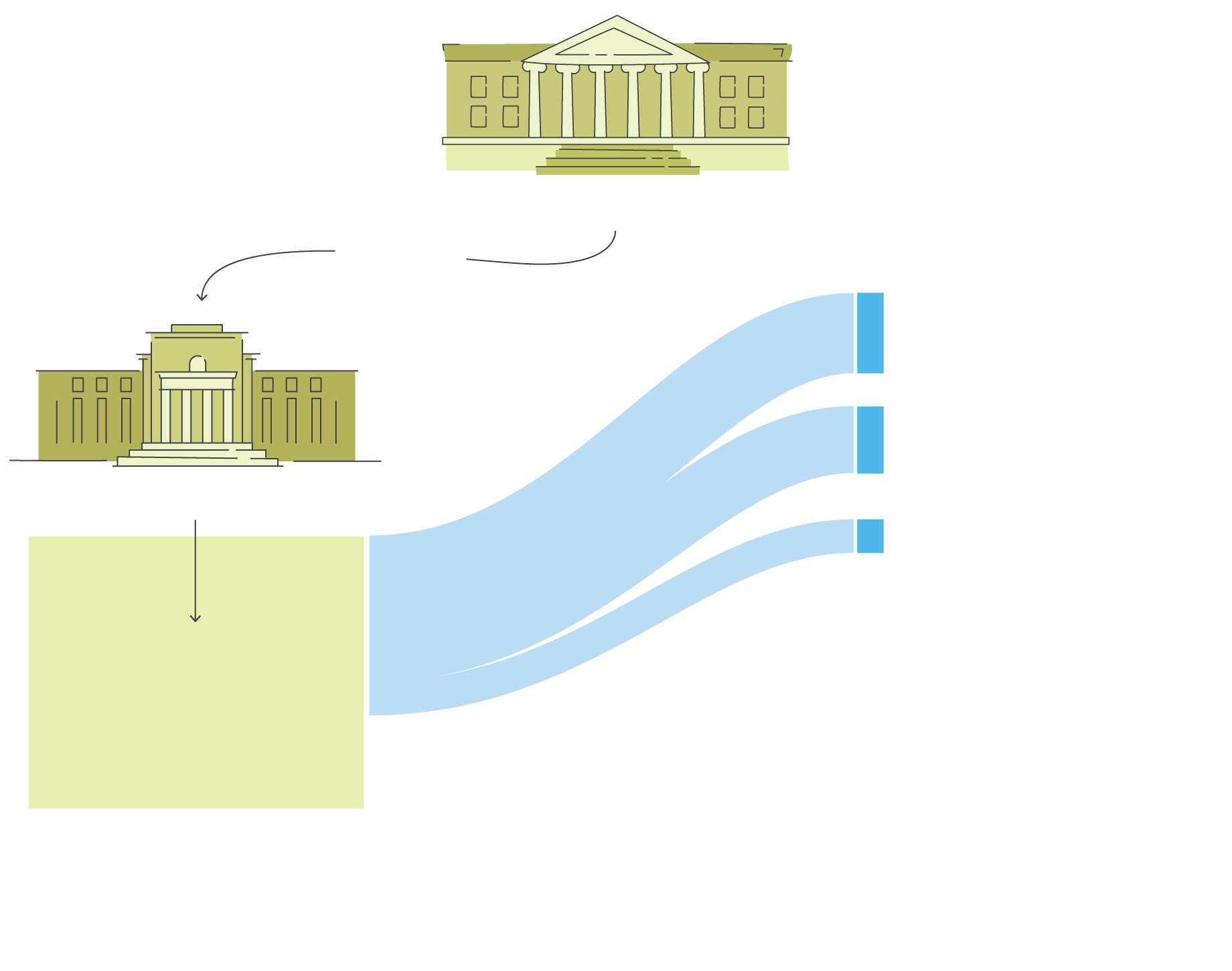

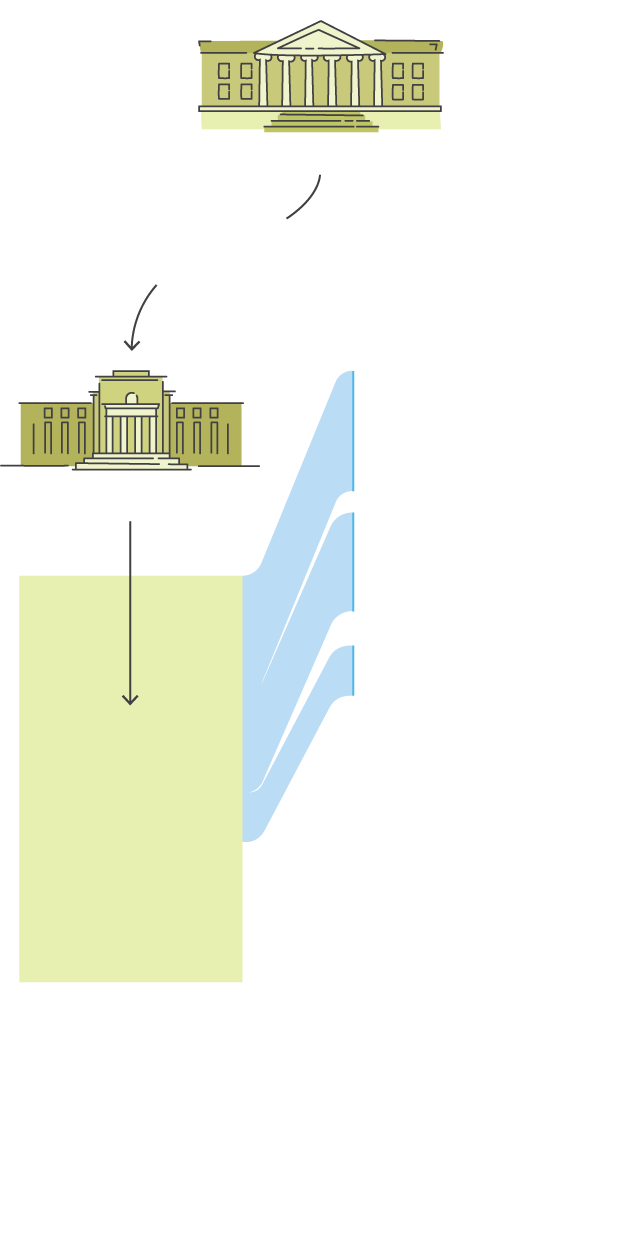

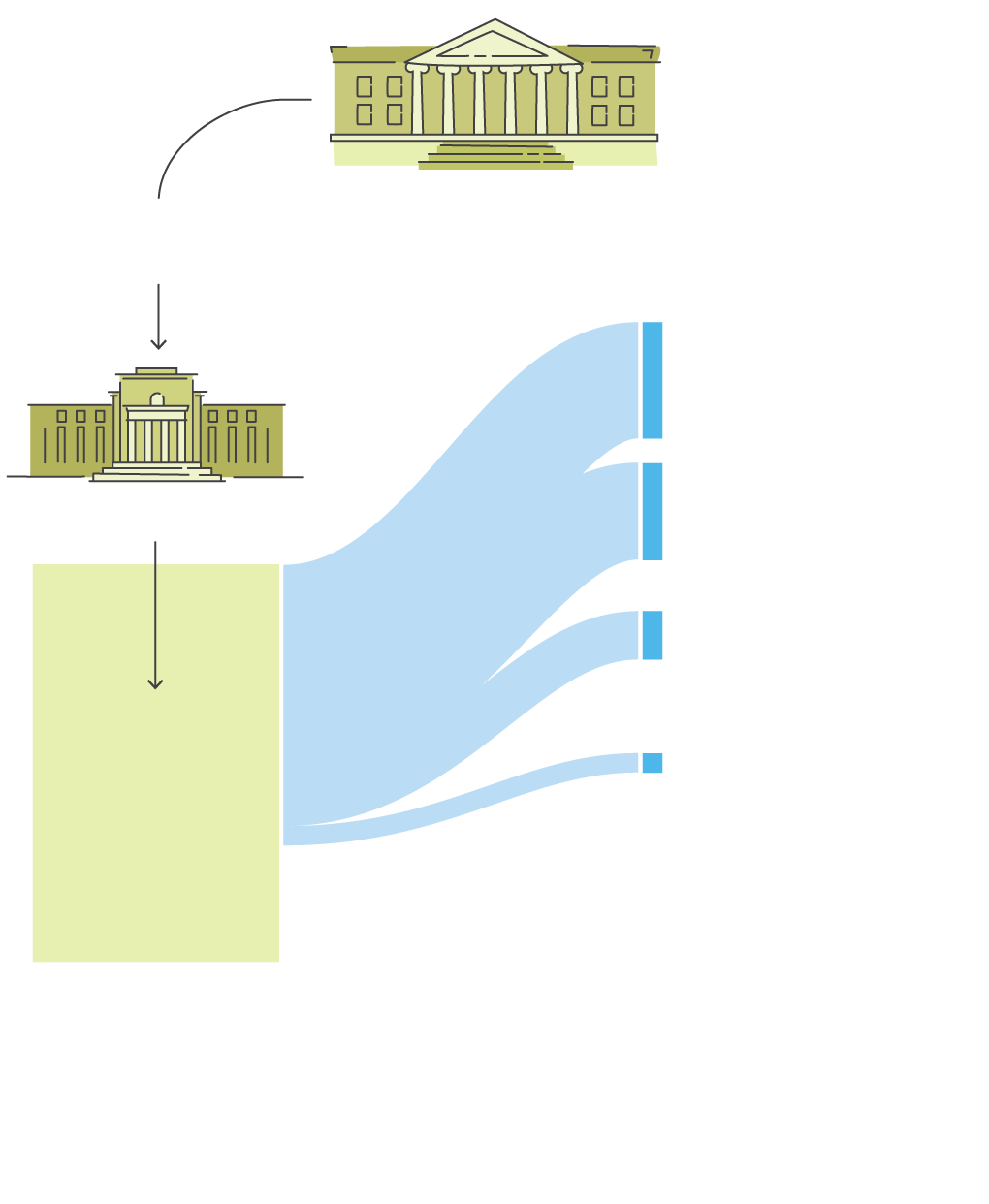

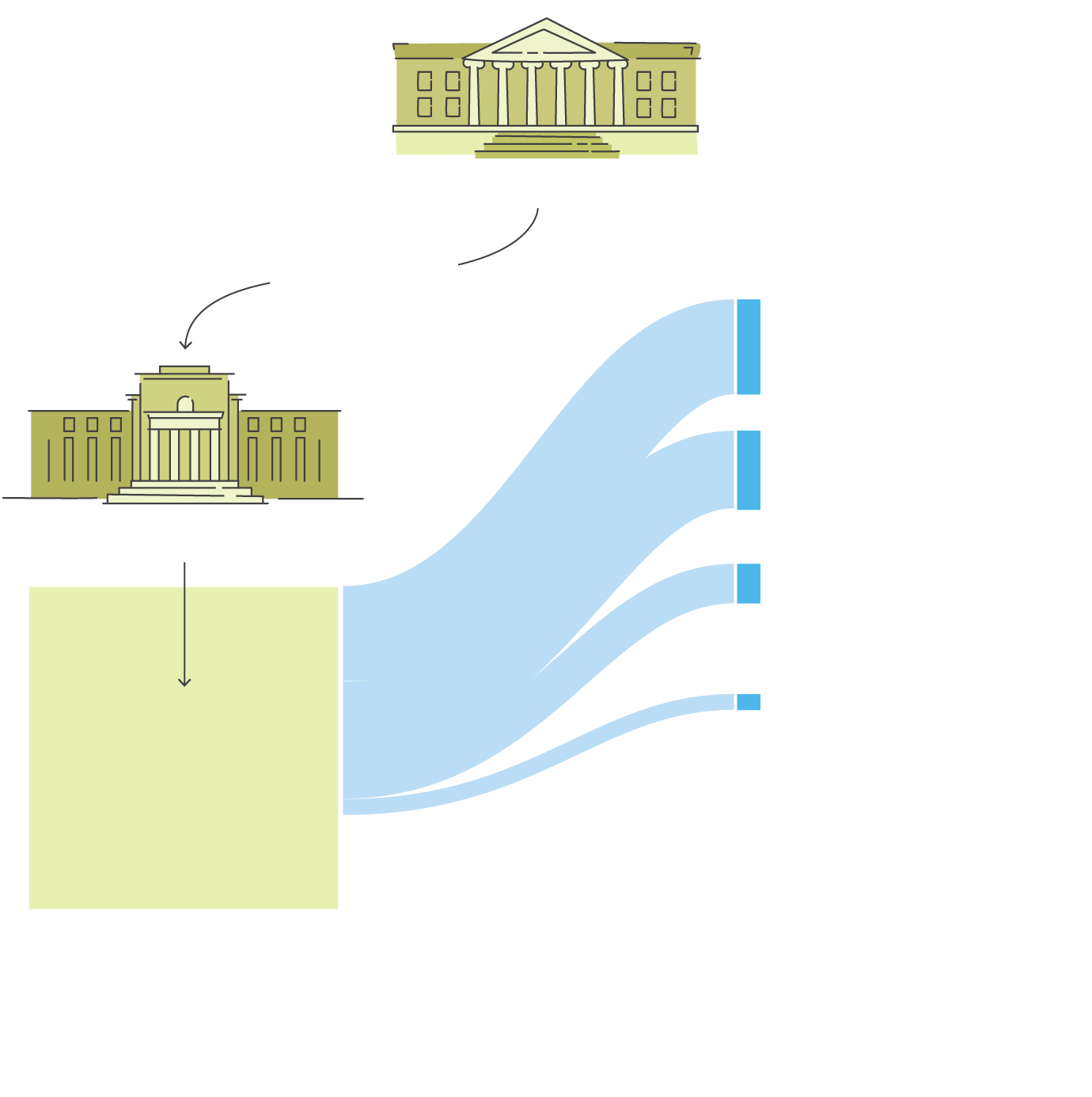

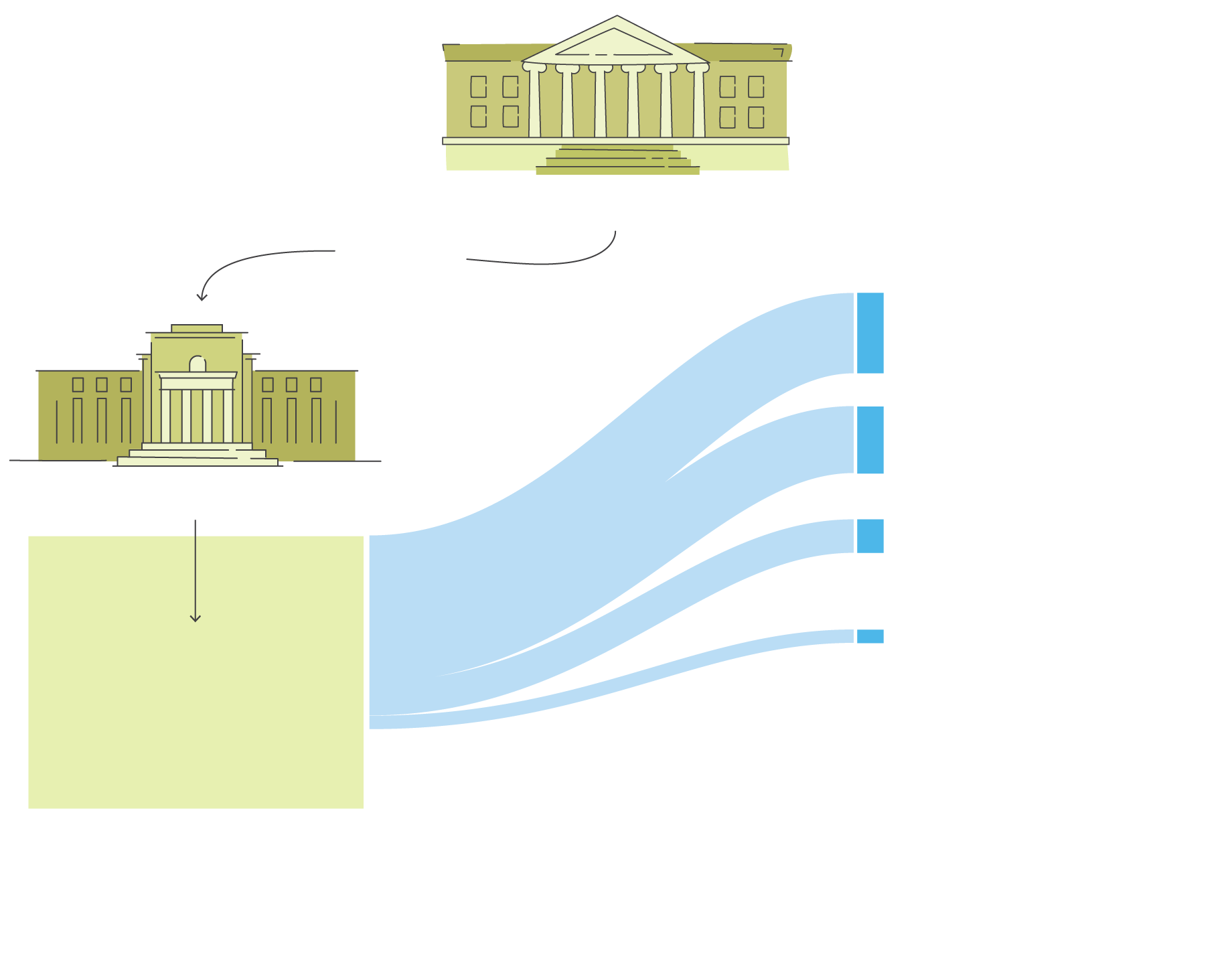

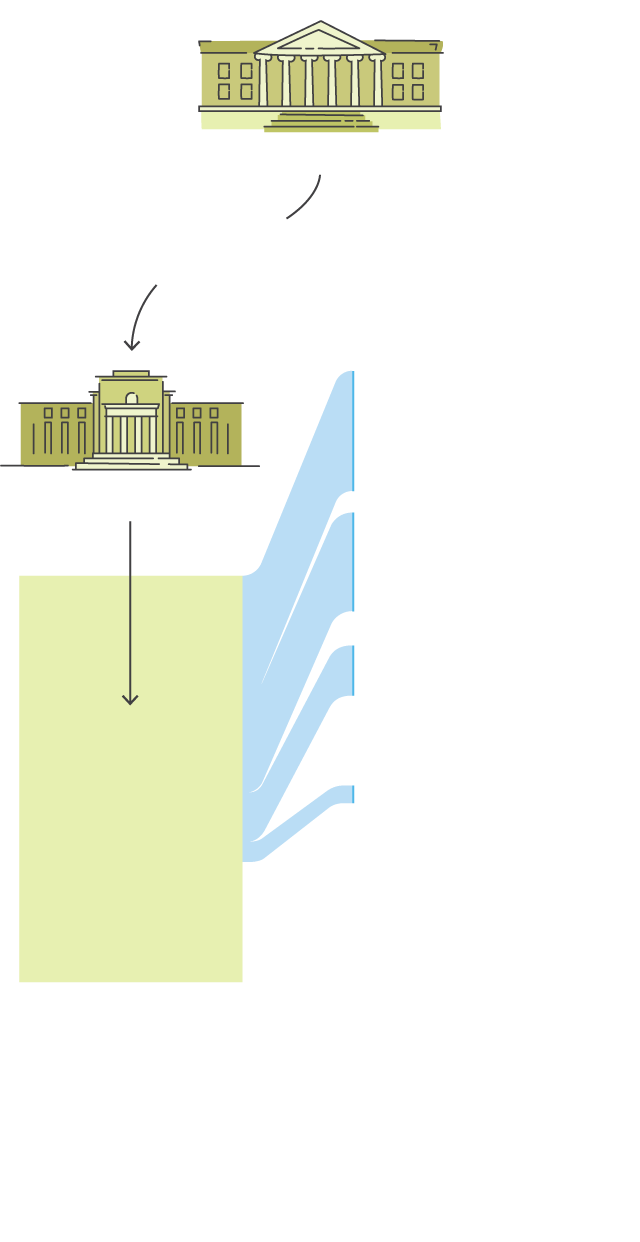

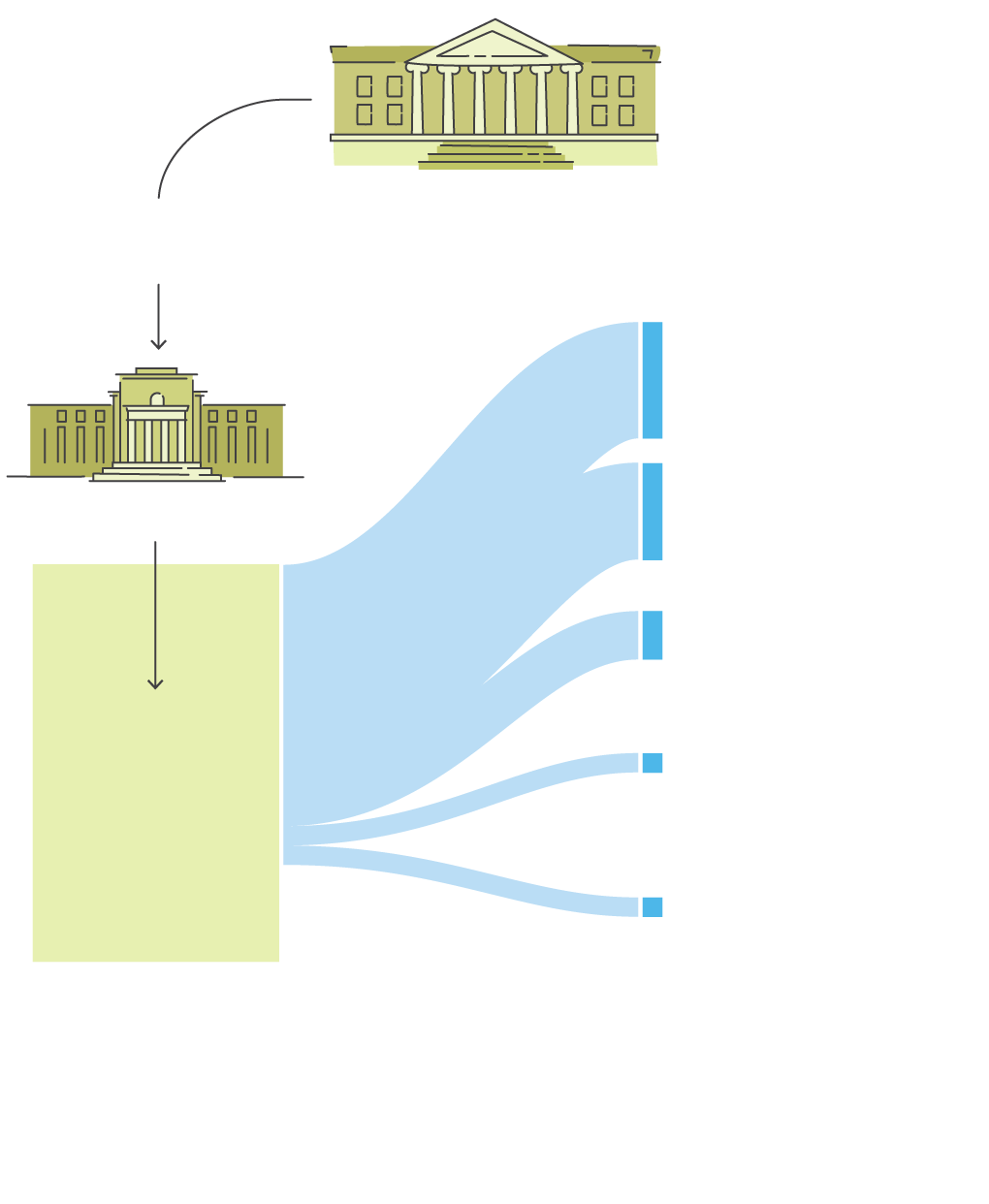

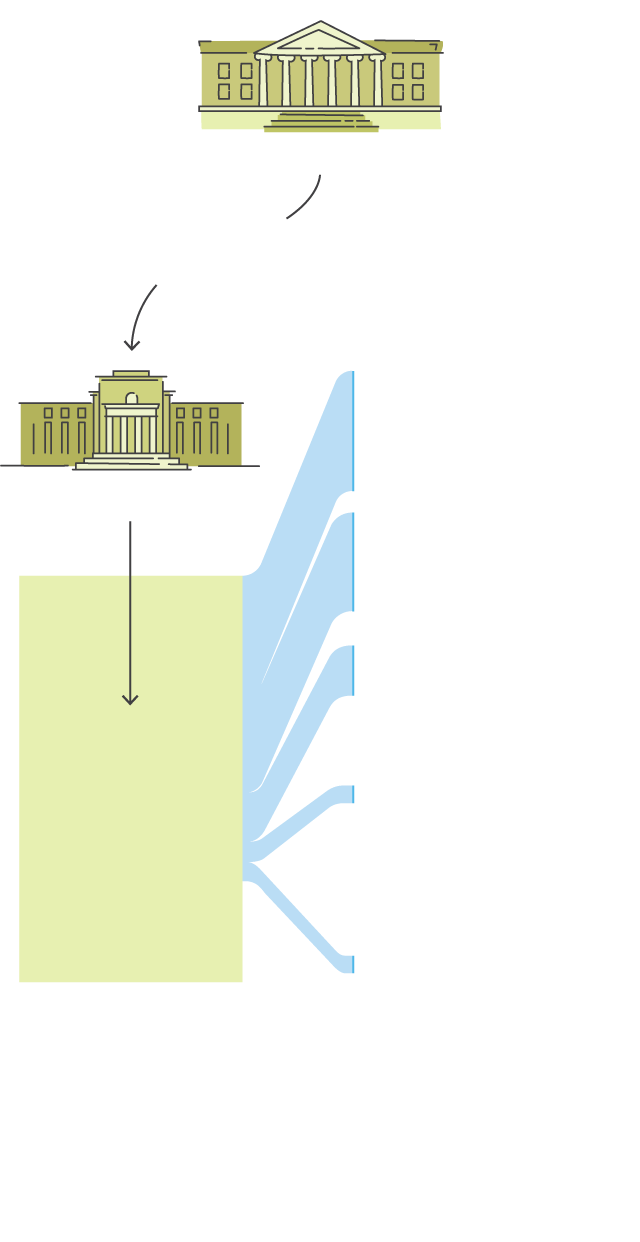

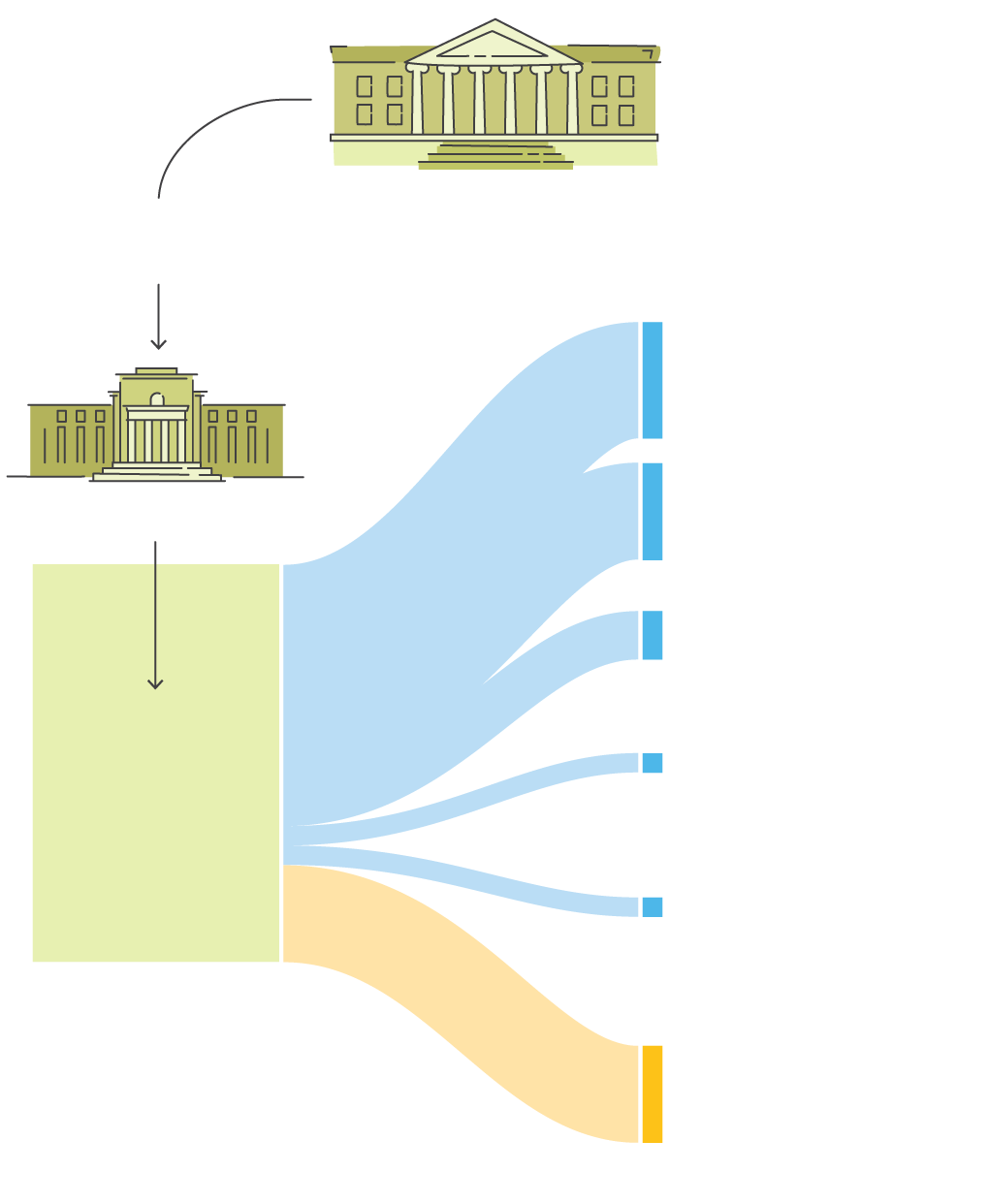

The U.S. Treasury Department and the Federal Reserve have set up roughly a dozen programs to keep people and businesses afloat during the coronavirus crisis, aimed at limiting bankruptcies, company failures, and family stress. The programs will funnel trillions of dollars to people and businesses left reeling as the economic consequences of the pandemic multiply.

The Treasury, the agency that collects taxes and pays the government’s bills, is responsible for the programs that are putting cash directly into the pockets of people and companies. The Federal Reserve is the nation’s central bank and an independent entity responsible for overseeing its money supply and financial markets. Its crisis programs help ensure people and companies, including banks and financial firms, continue to borrow and lend to each other, sometimes making those loans itself.

Here is how the Treasury- and Federal Reserve-backed aid breaks down:

Other federal programs

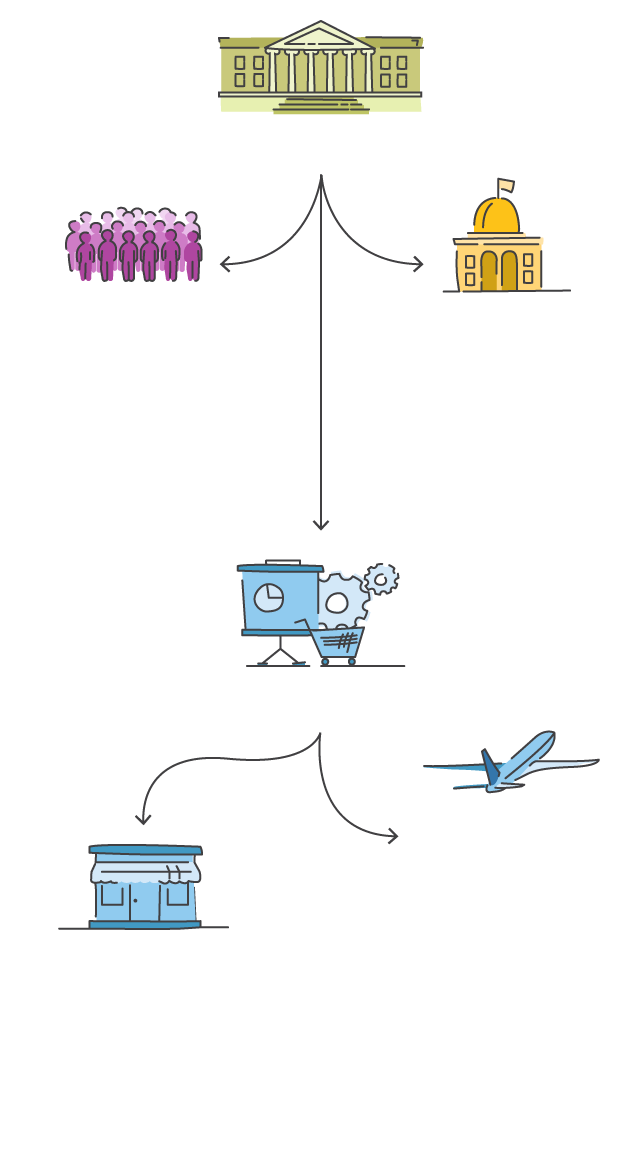

One of the Fed’s core purposes is to keep financial systems that function smoothly in normal times from grinding to a halt in a crisis.

That could be because of a traditional bank “run,” when depositors try to withdraw more cash than the bank has on hand, or because traders in key securities markets refuse to do business with each other.

In these cases it lends directly to banks and sometimes other financial institutions as a “last resort” source of cash when markets stop working normally.

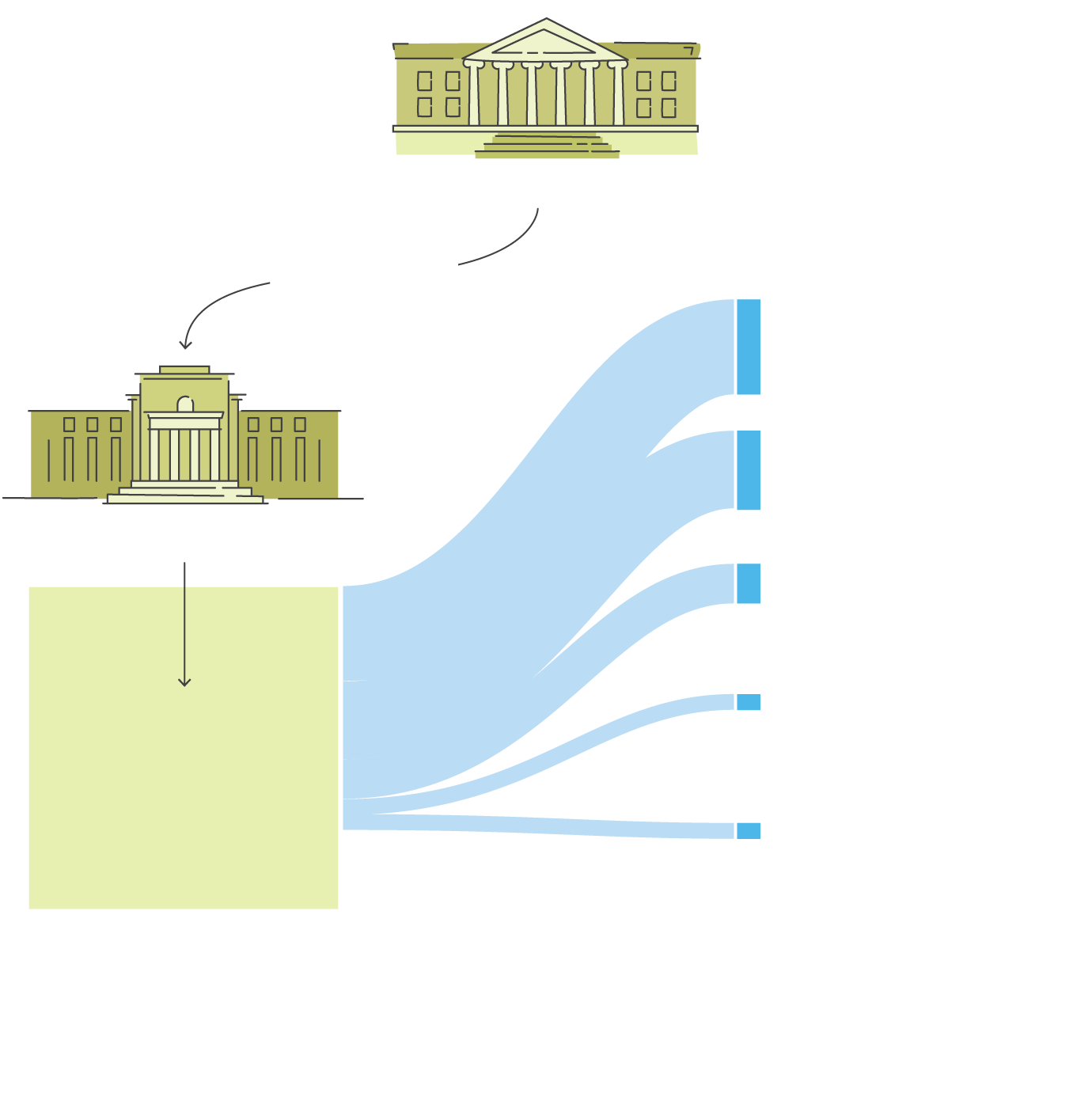

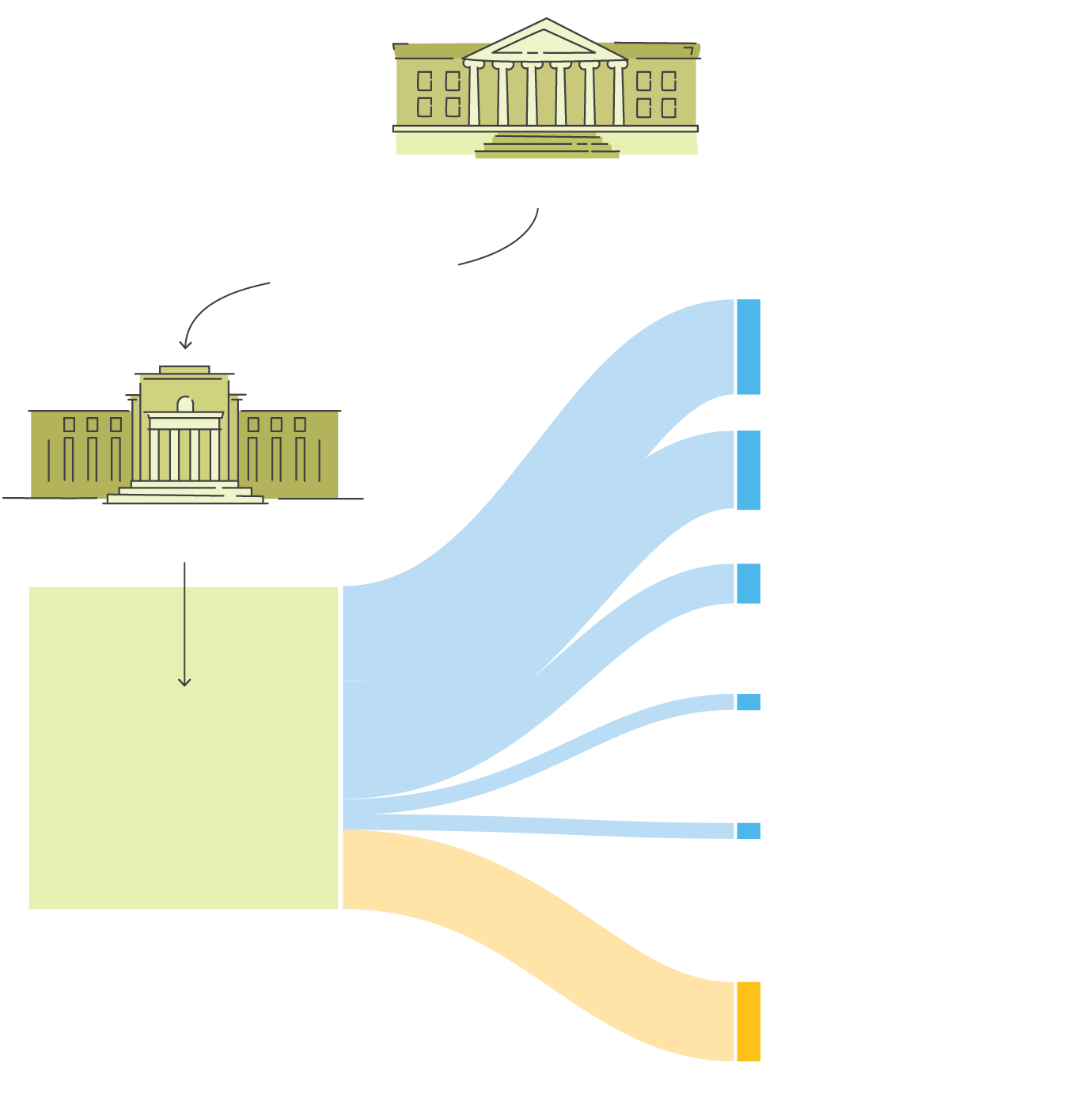

Money Market Mutual Fund Liquidity Facility

Prime money market funds are important management tools for large companies and institutions because they are considered a low-risk place to park cash. But if confidence erodes, demand for withdrawals can spike. The Fed makes sure those demands can be met.

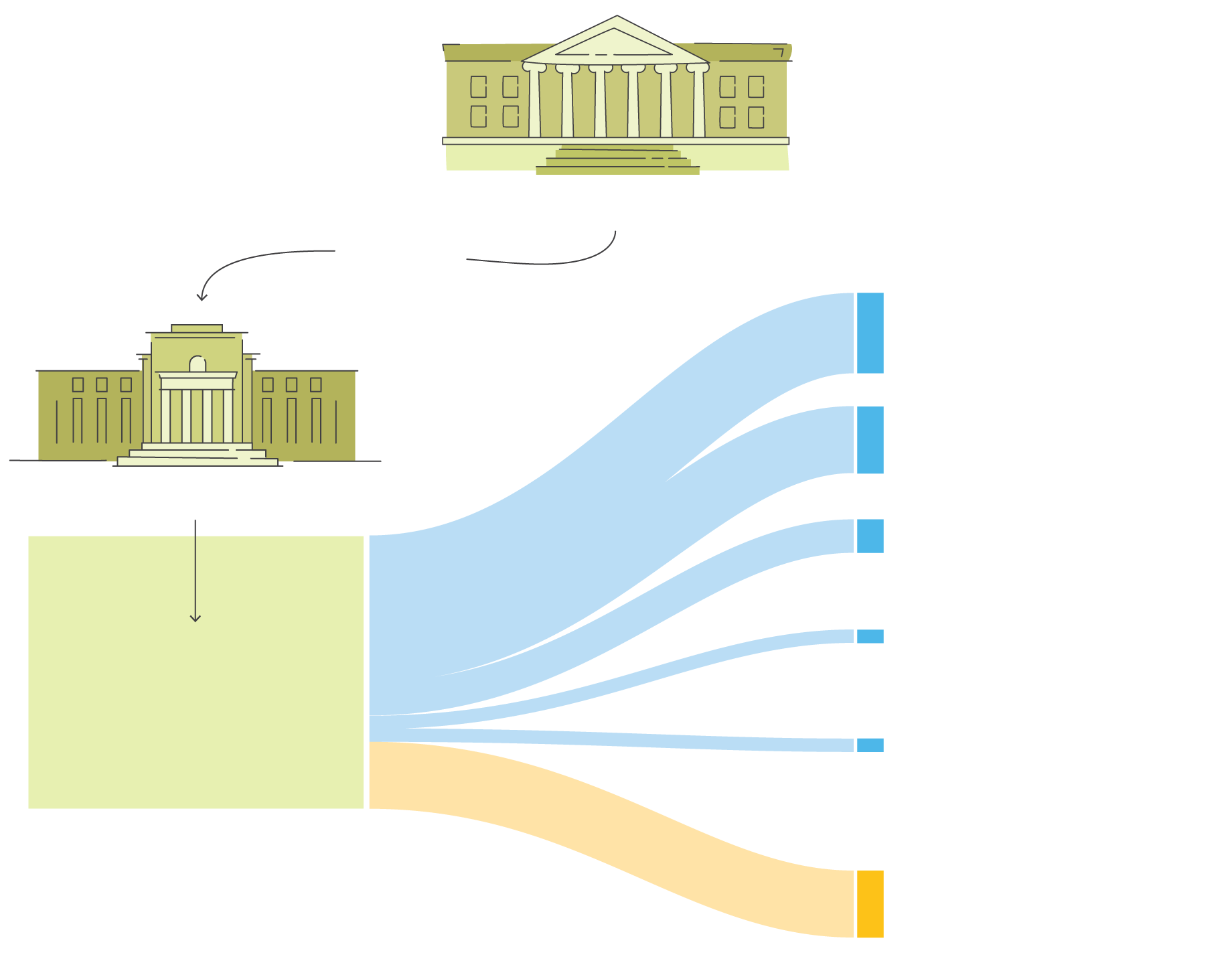

Primary Dealer Credit Facility (PDCF)

Restarts a program established after the 2008 financial crisis designed to provide overnight loans in exchange for eligible collateral.

The PDCF provides loans that settle the same business day and mature the following business day. The facility closed in 2010. The new PDCF offers loans with terms up to 90 days.

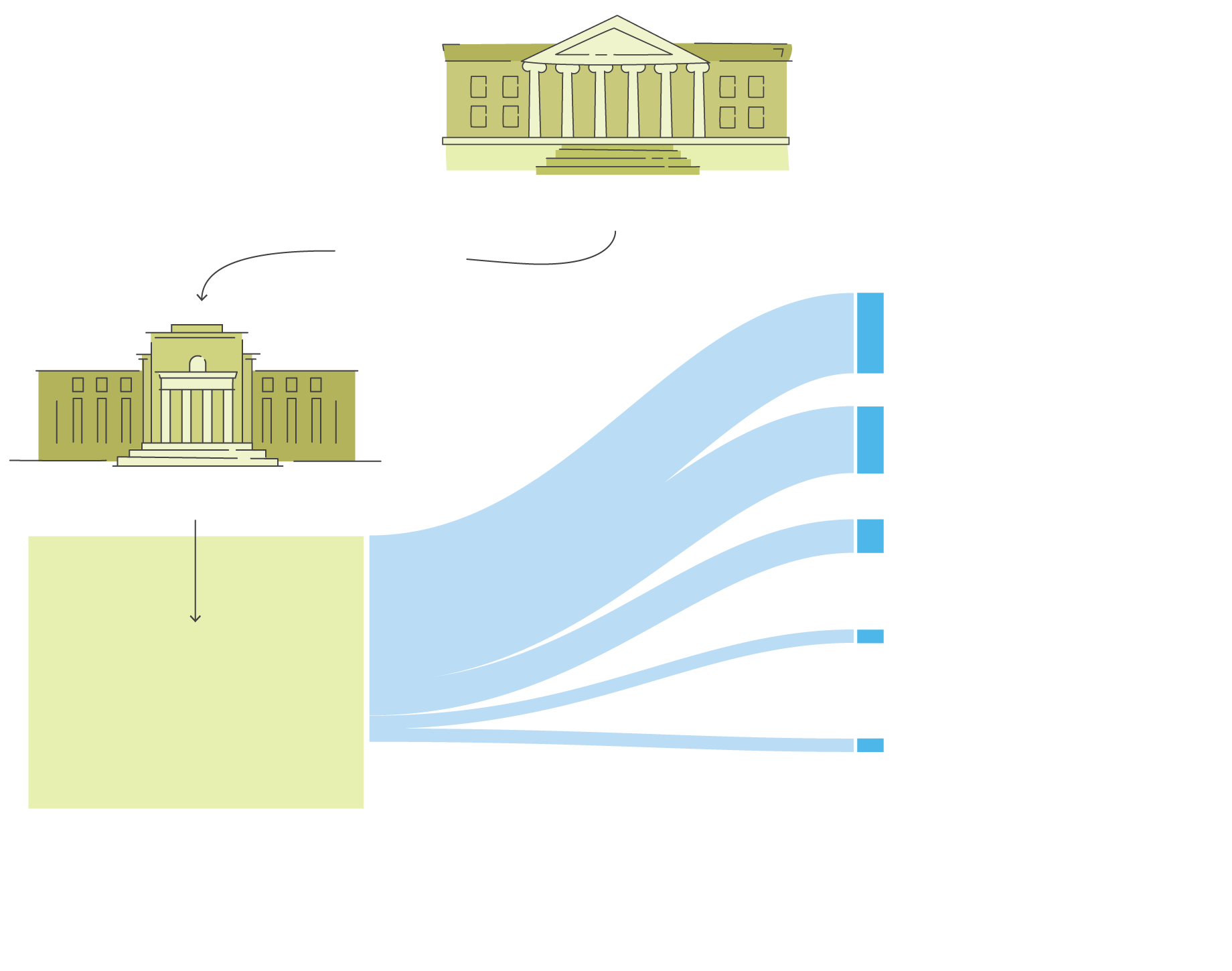

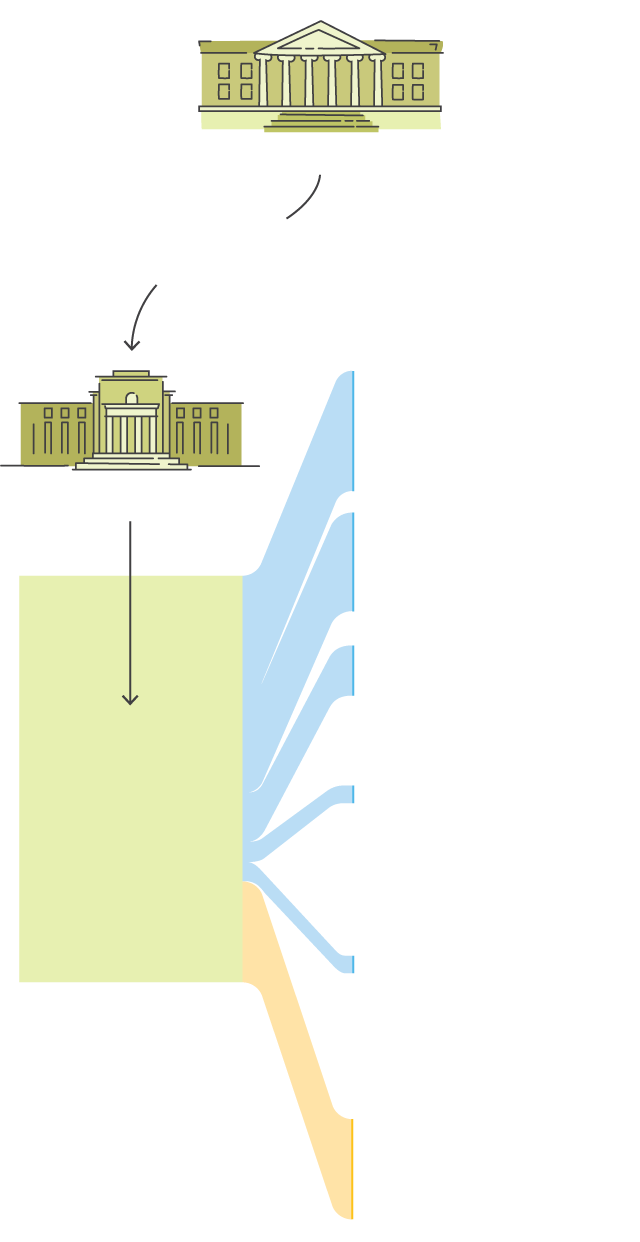

Quantitative Easing

Quantitative easing is when the central bank purchases longer-term securities from the open market in order to increase the supply of bank reserves and encourage lending. Its typical aim is to lower interest rates, but in this case Fed officials wanted to be sure the important global market for U.S. Treasury securities continues to function smoothly.

Discount Window

Banks that are unable to borrow from other banks in the fed funds market may borrow directly from the central bank’s discount window at the federal discount rate.

Swap Lines

The Fed has relationships with major foreign central banks to provide U.S. dollars in exchange for foreign currencies. It is also allowing other central banks to borrow dollars as long as they have U.S. Treasury securities to offer as collateral.

Sources: CARES Act; Federal Reserve